U.S. Macro Outlook

— updated 11.06.2024—

Fed Forward Guidance

Forward Guidance is a trap. It disables the Fed from changing its mind.

After a surge in unemployment due to COVID-19, the Fed decided to keep interest rates near zero until unemployment levels normalized. But even as inflation surged beyond the 2% target, the Fed seemed unable to alter course, and near-zero interest rates persisted.

There is also an effect when guidance is rapidly altered. Rapid rate hikes leading up to March 2023 massively devalued SVB’s long-term bond portfolio. Tangentially, the failure of the Fed to address smaller banks with the same rigor as the SIBs led to SVB’s failure. Their Common Equity Tier 1 (CET1) ratio did not account for mark-to-market losses. In other words, the regulations did not consider unrealized losses in SVB’s long-term bond portfolio.

Now, we see the same issues with Fed forward guidance. Though the short-term economy is performing well by many metrics (low unemployment, rallying equity markets, tight credit spreads), the Fed made the hasty decision to cut rates by 50 bps and is pondering two more rate cuts by year-end. At some point, you have to ask if Fed forward guidance is materially beneficial. In other words, is a macroeconomy guided by the Fed better than the counterfactual?

Short-Term vs. Long-Term Dissonance

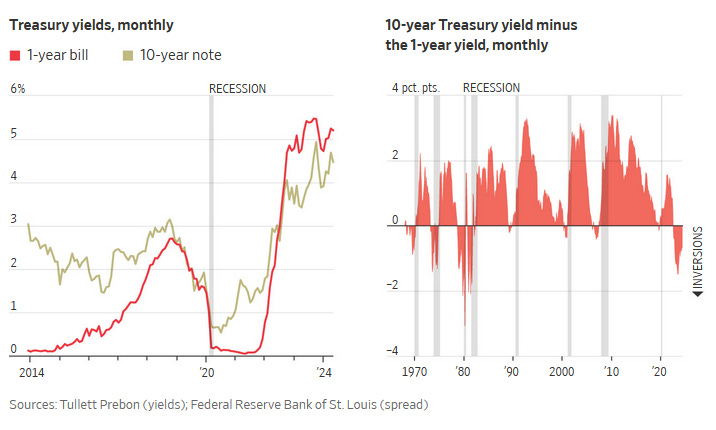

There seem to be two different economic outlooks at the moment. The short-term looks rather attractive from an investor’s perspective. Record equity prices, a 50 bp rate cut that is beginning to fuel economic activity, record low unemployment, and a normalizing yield curve (see the rise in 10-year yields).

However, the market has seemingly simultaneously priced in long-term inflationary expectations and economic uncertainty. This is evidenced in the prices of gold and Bitcoin rallying recently, in part due to the declining rate environment. The inclusion of these “safe” assets as hedges against economic volatility in many portfolios falls in line with my analysis throughout the last few months.

I noted it briefly in June, but the normalization of the yield curve, covered extensively by Bravos Research, may be at play here. Many of the patterns in equity appreciation, inflation, and employment that have resulted in prior recessions seem to be emerging in the present. I should note that recessions often lag behind yield curve normalization. That is, recessions occur (generally) hundreds of days after the yield curve normalizes.

Weak signs, at pressing times…

The Nikkei 225, Japan’s hallmark stock market index, has just hit a 40-year low. This sudden decline is emblematic of a broader global market downturn. In the United States, a flimsy jobs report, slow economic growth, and decreasing consumer purchasing power (see earlier entry) have set a rather troublesome macroeconomic scene.

The triumphs of the MAG 7 throughout the better part of 2024 have seemingly been corrected, as Nasdaq indexes follow suit with their peers. These triumphs were largely achieved because of widespread hype around generative AI development: over 50% of VC investment in Q1 ’24 went to AI/ML startups. Whereas data quality and algorithmic capabilities have largely remained unchanged, AI compute has grown tremendously. This surge in compute is reflected by Nvidia’s historic run and mass sale of H100-powered GPU clusters.

But the market has priced in the hype, and the global macroeconomic outlook looks bleak. Now, all eyes are on the Federal Reserve and its Chair Jerome Powell for some long overdue interest rate cuts.

All this, not to mention the dire state of the American real estate market.

I keep this analysis brief because it isn’t novel or contrarian. But it is real and deserves some attention, especially from the current Biden-Harris administration.

With the presidential election just months away, and the odds seemingly rebalancing in VP Kamala Harris’s favor, it appears that economic recourse is imminent.

Consumer Savings -> Implication on GDP -> Revenues vs. Costs -> Poor Economic Outlook

In May, the San Fransisco Fed published data showing that the savings Americans obtained throughout the COVID-19 period were depleted. These “excess savings” were no more.

This data is generally alarming. American spending emanates from two sources: savings and credit. If savings are depleted, consumers are more likely to purchase via credit, adding to the record $1.1 trillion aggregate credit card balance reported in Feb. 2024. However, it is even more alarming when paired with some context.

Spending by consumers accounts for roughly 70% of GDP. To put that into perspective, World GDP is constituted by about 15% consumer spending.

Now, zoom out to GDP on the whole. GDP growth in Q1 ’24 was 1.3% on an annualized basis. Think of that as the growth rates of revenues in the country.

How, then, are costs growing relative to revenue?

Last week, the Labor Department reported that the CPI held at 3.3%, just under the expected 3.4%. This figure, edging closer to the Fed’s target 2% and minuscule compared to the 9.1% experienced in June ’22, along with U.S. unemployment data have garnered some global optimism about America’s economic health.

But, amid concerns of U.S. debt financing, unknowns surrounding the upcoming presidential election, and signs of a weakening labor market, it is hard to say that the U.S. economic outlook is strong.

Interest rates are another cost. With the Fed not looking to cut rates until inflation subdues further, the cost of borrowing remains high making investment lethargic.

The bottom line is that there just isn’t enough growth relative to persisting costs.

Another tidbit regards the inverted U.S. Treasury yield curve, which has been inverted for the longest period on record. Historically, the normalization of these yield curves has resulted in a recession. As rates normalize and treasury yields get priced accordingly, a looming recession remains a threat.